China weekly: Steel prices edge lower amid weak consumption, ample supply

-

- Weak seasonal demand continues to pressure China steel prices.

-

- Rising inventories and excess supply weigh on market.

China’s crude steel production fell 2.7% y-o-y to 84.36 million tonnes (mnt) in May, according to industrial statistics released by the National Bureau of Statistics (NBS) on 16 June. Average daily crude steel output stood at 2.721 mmt, down by around 60,000 tonnes (t) from the previous month. However, concerns over excess production continue to persist amid weak domestic demand in China.

According to the China Iron and Steel Association (CISA), total steel inventories at key CISA-affiliated mills stood at approximately 16.87 mnt during (1-11) June 2026, increasing by 1.04 mnt or 6.6% from 15.83 mnt recorded in late-May. The increase in inventories coincided with a recovery in crude steel production during the period, while downstream demand remained relatively subdued, resulting in higher stock accumulation at mills. On a y-o-y basis as well, inventories were up by approximately 1.08 mnt or 6.8% compared with 15.79 mnt the same period last year.

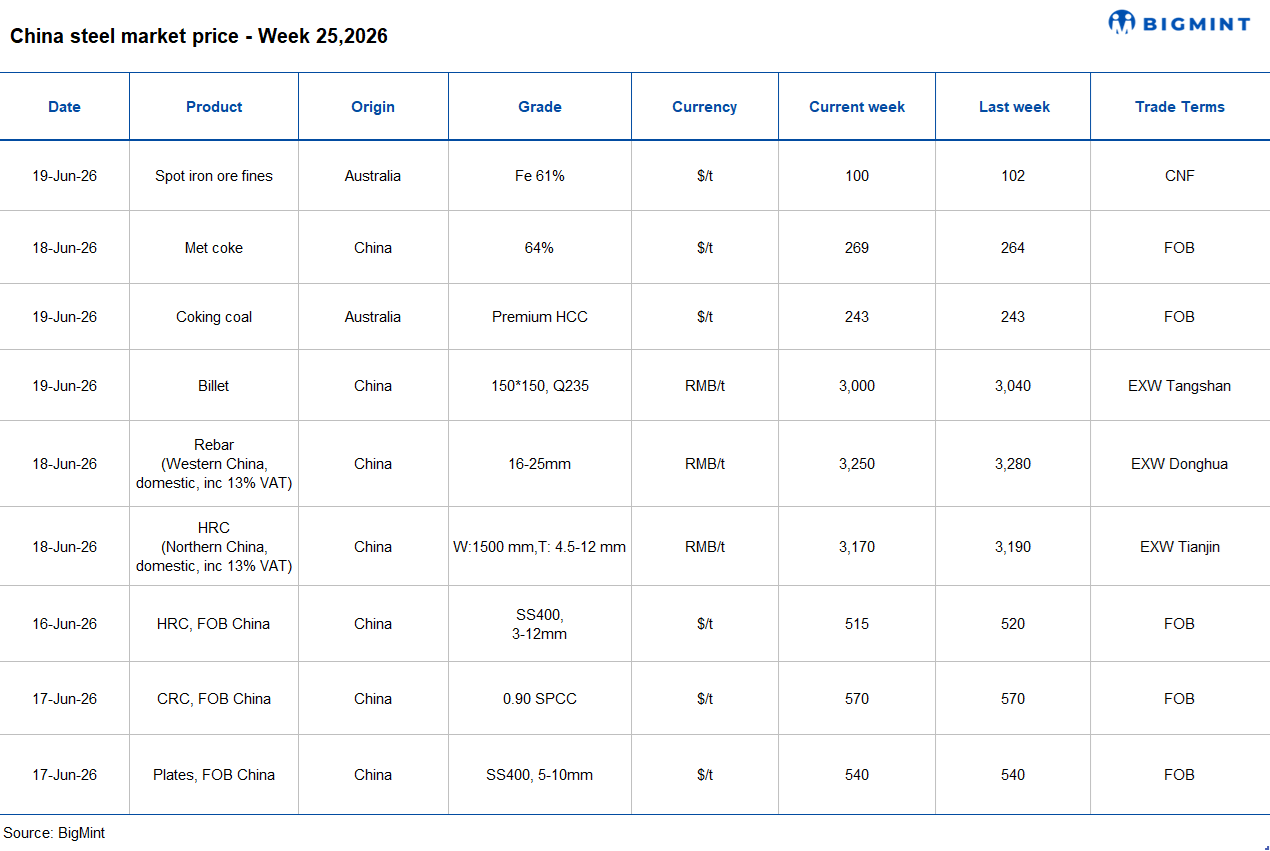

China’s steel prices show downward trend in the week ended 19 June 2026. Chinese HRC and rebar prices dropped with the market facing a seasonal slowdown. On the raw materials front, prices of iron ore and billet prices stable, though coke prices increased w-o-w.

Raw material prices:

Iron ore spot prices drop w-o-w: Iron ore fines benchmark prices for Fe 61% decline w-o-w by $1/t w-o-w to $100/dmt CFR China on 18 Jun’26 compared with $101/t on 11 Jun’26.

Prices lost strength amid growing pressure from weak steel demand and shrinking mill margins in China. The decline was mainly linked to continued weakness in China’s steel sector, which is currently in its seasonal off-season period. Heavy rainfall across southern China disrupted construction activity and slowed finished steel consumption, reducing demand for raw materials. Moreover, chances of a near-term recovery in steel demand remain low, keeping iron ore sentiment weak.

a) Spot pellet premium steady w-o-w: Spot pellet premium for Fe 65% grade pellet remained largely stable at $19.60/t CFR China on 17 June.

b) Spot lump premium rose w-o-w: Spot lump premium edged up w-o-w by $0.017/dmtu to $0.1990/dmtu on 18 June.

Coking Coal Market Remains Firm Amid Supply Constraints and Stable Steel Demand: China’s coking coal market stayed firm during the week, supported by tighter supply due to stricter safety checks and temporary mine closures in key producing regions. Limited raw coal availability impacted coke output, while low inventories and strong blast furnace operations continued to support market sentiment. The start of the eighth round of coke price hikes further reflected market strength.

Australian Premium Hard Coking Coal (PHCC) prices remained stable w-o-w to $243/t FOB Australia as geopolitical risks softened, which reduced supply risk concerns. BigMint’s coking coal index also declined slightly by $1/t to $267/t amid muted trading activity.

Billet prices decline w-o-w amid weak demand:Chinese billet prices fell to RMB 3,000/t ($444/t) on 18 June from RMB 3,040/t ($424/t) on 12 June, pressured by seasonally weak steel demand, rising social inventories, and cautious market sentiment. Although mills maintained relatively firm pricing due to elevated production costs, the market remained under pressure from sluggish domestic consumption and subdued trading activity. Support from raw material costs weakened during the week as iron ore prices slipped below $100/t amid ample port inventories and increased supply from alternative origins. Meanwhile, rising coke and coking coal prices continued to support production costs and limit sharper billet price declines.

Chinese billet export offers were heard at around $470/t FOB throughout the week, reflecting stable export sentiment despite limited trading activity and cautious overseas buying interest. Export demand remained subdued, while increasing competition in the semi-finished steel market continued to weigh on fresh bookings. Trading activity is likely to remain limited due to the Dragon Boat Festival holiday in China from 19-21 June.

Steel prices trend:

Rebar prices decrease w-o-w: Rebar prices in China were down by RMB 30/t ($4/t) w-o-w to around RMB 3,250/t ($480/t) as on 18 June, compared with RMB 3,280/t ($484/t) in the previous week. Furthermore, SHFE rebar futures (October 2026 contract) also dropped by RMB 39/t ($6/t) w-o-w to RMB 3,134/t ($463/t) as on 18 June from RMB 3,173/t ($469/t) a week earlier.

China’s domestic rebar market remained under pressure in mid-June as seasonal demand continued to weaken. Slower construction activity and high inventory levels at both steel mills and in the market limited buying interest, keeping rebar prices subdued. At the same time, lower profit margins led some steel mills to increase maintenance work and cut production. As a result, blast furnace operating rates edged down slightly, reflecting efforts by mills to reduce supply, control inventories, and manage costs in response to softer market conditions.

Additionally, economic data released this week for the January-May period highlighted continued weakness in the real estate sector and fixed-asset investment, resulting in further softness in downstream demand.

Domestic HRC prices decrease w-o-w: Chinese HRC prices decreased by RMB 20/t ($3/t) w-o-w to around RMB 3,170/t ($468/t) on 18 June from RMB 3,190/t ($471/t) from the previous week. Moreover, SHFE HRC futures (October 2026 contract) edged down by RMB 23/t ($3/t) w-o-w to RMB 3,351/t ($495/t) from RMB 3,374/t ($498/t) a week earlier. Additionally, China’s HRC export offers dropped by $5/t w-o-w to around $515/t FOB Rizhao compared with $520/t from the previous week.

China’s HRC prices edged lower this week as weak seasonal demand and cautious purchasing continued to weigh on the market. Lower purchasing activity led to a further buildup in inventories, while increased HRC production added more supply to the market. As a result, HRC prices moved lower during the week. However, the drop was not significant, as higher coking coal and metallurgical coke prices helped support steel production costs. Even so, weak demand and rising inventories continued to put pressure on HRC spot prices.

Chinese HRC export prices declined this week as overseas buyers held back from purchases, expecting lower freight costs and cheaper steel prices in the coming weeks. The cautious buying sentiment reduced trading activity and put pressure on export prices.

Outlook:

China’s steel market is expected to remain largely stable with a slight downward bias in the coming week. Seasonal rainfall across several regions is likely to limit construction activity and keep demand subdued. However, if export demand improves, the decline in steel prices may be limited, helping the market remain relatively stable.