Weekly round-up: Monsoon caution weighs on steel markets amid mixed price trends

- Weak demand and monsoon disruptions kept steel procurement sentiment cautious.

- Ferro alloys strengthened on costs, while semis and longs stayed mixed.

Semi-finished markets remained mixed amid monsoon-led demand weakness, while long steel prices stayed under pressure despite regional resilience. Ferro alloy prices strengthened on elevated production costs, tighter availability, and improving export demand.

Iron ore and pellet:

- In OMC’s 19 Jun’26 auction, around 90% of 1.14 mnt iron ore lumps (Fe 60-65%) were booked at INR 4,750-7,300/t, with premiums of up to 19% over base prices. However, weighted average bids declined by INR 250/t m-o-m despite stable base prices. Meanwhile, 76% of 2.01 mnt iron ore fines (Fe 51-65%) offered received bids at INR 3,500-5,850/t, with premiums of around INR 100/t over base prices. Weighted average bids for fines edged up by INR 50/t m-o-m

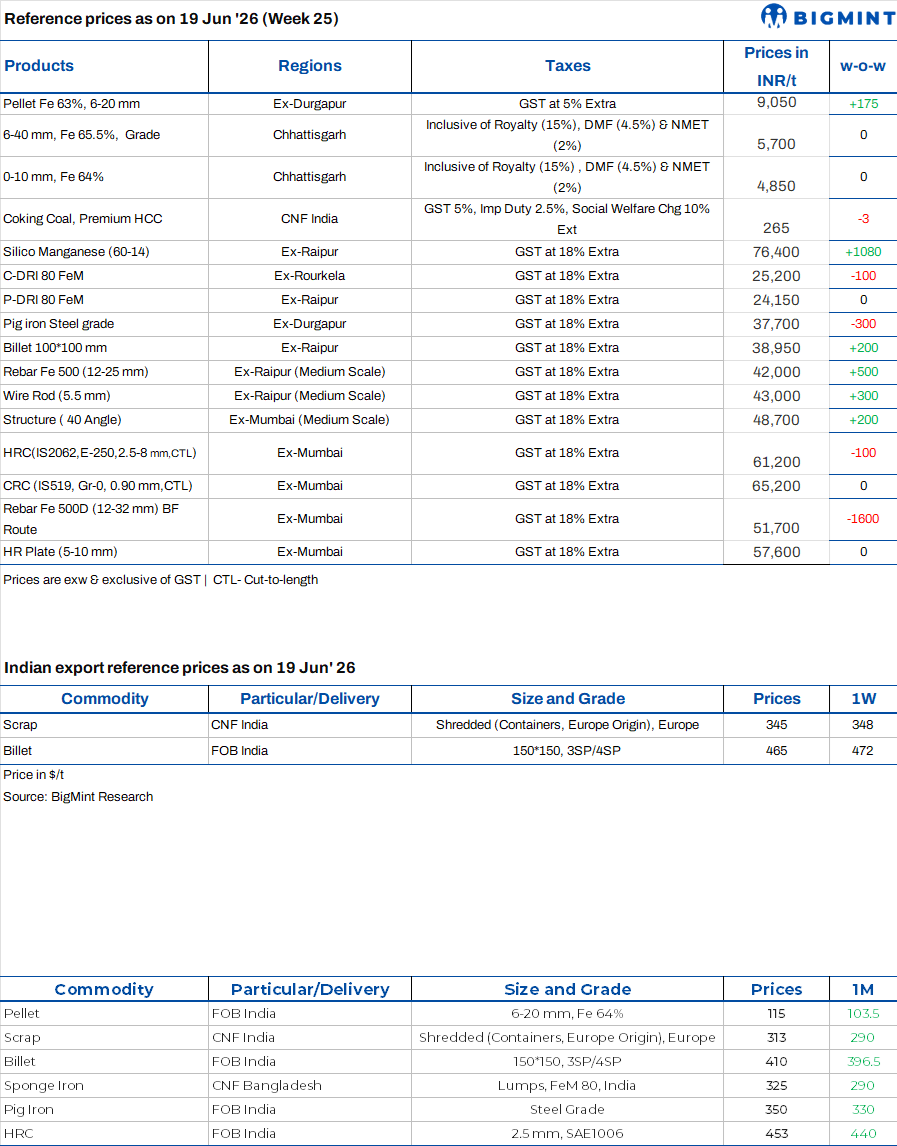

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, decreased by INR 700/t to INR 8,900/t ($94/t) DAP. Pellet prices in the Raipur region witnessed a sharp correction this week after local pellet manufacturers reduced their offers by around INR 400/t a few days ago. The price decline attracted strong buying interest from steelmakers, resulting in significant bulk trade activity across the market.

- During SAIL auctions held from Monday to Thursday, around 68,000 t of iron ore (Fe 61.8-62.64%) was booked at prices ranging between INR 5,225-5,800/t. The prices were on an ex-mines/FOR loaded into rake basis, inclusive of royalty, DMF, NMET, and additional premium charges.

Coal:

- BigMint assessed RB2 (5,500 NAR) at INR 11,000/t ex-Paradip, down INR 50/t w-o-w, while RB3 (4,800 NAR) declined by INR 200/t to INR 9,700/t. At Vizag, RB2 prices fell to INR 10,800/t, while RB3 declined to INR 9,750/t. Portside coal inventories across major Indian ports declined by 5.7% w-o-w to 14.72 mnt, indicating improved evacuation activity. However, lower spot demand continued to weigh on supplier sentiment, with CNF Gangavaram RB2 assessed at $113/t, down $5/t w-o-w. Market participants reported vessel offers near $110/t, reflecting increasing pressure on sellers to remain competitive.

- Indias domestic non-coking coal prices remained stable during the week, supported by sufficient availability and cautious buying behaviour. BigMint assessed 5,000 GCV coal at INR 5,500/t and 4,500 GCV coal at INR 4,050/t, both exw-Bilaspur. Eastern Coalfields Ltd (ECL) recorded limited participation in its 11 June e-auction, allocating only 106,400 t against nearly 0.8 mnt offered, resulting in an allocation ratio of just 13.3%.

- BigMint’s premium hard coking coal (PHCC) index was assessed at $267/tonne (t) CNF Paradip, India, on 19 June 2026, down by $1 w-o-w. Sufficient inventories and drop in steel prices have held back Indian mills from bidding aggressively for coking coal.

- On the other in the recent development this week Bharat Coking Coal Limited (BCCL) transferred its 2 mnt/year Dugda Coal Washery to JSW Steel, marking India’s first coal washery monetisation initiative. The development represents a significant step towards improving coal beneficiation capacity, enhancing washed coal availability, and encouraging private participation in coal infrastructure. The initiative is expected to support better utilisation of existing assets while strengthening the supply chain for the steel industry.

- India’s imported met coke market improved during the week ended 18 June, supported by firm international coke prices and rising raw material costs. Indonesian BF-grade met coke (65/63 CSR) increased by around $3/t w-o-w to approximately $318/t CFR India, reflecting stronger supplier offers.

- In contrast, the domestic BF-grade met coke market remained stable due to comfortable availability and balanced demand-supply conditions. Eastern India prices declined slightly to INR 36,500/t ex-Jajpur, while western India remained steady at INR 34,000/t ex-Gandhidham. The divergence between imported and domestic markets highlights stronger global cost pressures, while domestic supply conditions continue to limit price increases.

Ferrous Scrap:

- Imported ferrous scrap market remained subdued throughout the week, with weak steel demand, poor import viability, and the availability of cheaper domestic alternatives such as sponge iron, DRI, and busheling scrap continuing to weigh on buying sentiment. Mills largely stayed away from fresh bookings and focused on immediate requirements.

- A wide bid-offer gap persisted, with HMS 80:20 offers largely heard at $340-355/t CFR and shredded scrap at $380-395/t CFR, while buyers targeted lower workable levels of $330-340/t CFR for HMS and $350-375/t CFR for shredded scrap. Demand for shredded scrap in southern India remained particularly weak amid ample availability of lower-cost domestic feedstock.

- In the last seven days, around 3,500-4,000 t of imported ferrous scrap was booked for India, including HMS 80:20, LMS bundles and Turning Turnings scrap.

Ferro alloys:

- Silico Manganese:Indian silico manganese (60-14) prices increased by INR 875/t ($9/t) w-o-w to INR 76,100-77,000/t ($807-816/t) across key markets.Prices were supported by elevated production costs as major producers continued using high-cost manganese ore inventories acquired in April 2026, while stronger export demand improved acceptance of higher offers.

- Meanwhile, HC 65-16 silico manganese export prices rose by $5/t to $923/t FOB Vizag/Haldia.

- Additionally, SMIORE’s 15 Jun’26 manganese ore auction recorded 17% bookings, with bids increasing by up to 11% compared to the 5 Jun’26 auction.

- Ferro Manganese:Indian ferro manganese (70%) prices rose w-o-w by INR 600/t ($6/t) to INR 79,000/t ($825/t) in Raipur and by INR 700/t ($7/t) to INR 79,000/t ($825/t) in Durgapur. Prices increased as sellers resisted lower bids amid limited spot availability and firm production costs, prompting buyers to accept slightly higher transaction levels.

- Meanwhile, export prices for the 75% grade also went up by $7/t w-o-w to $918/t FOB Vizag/Haldia.

- Ferro Silicon:India ferro silicon (Si 70%) prices fell by INR 600/t ($6/t) w-o-w to INR 94,500/t ($1,002/t) ex-works Guwahati, while Bhutan prices also fell by INR 1,700/t ($18/t) to INR 94,000/t ($996/t). Prices fell amid bid-offer disparities, which forced sellers to reduce offers.

- Ferro Chrome:India high-carbon ferro chrome (HC 60%, Si 4%) prices remained steady with a slight rise of INR 700/t ($7/t) w-o-w to INR 123,200/t ($1,306/t) ex-works Jajpur. Market witnessed a slight improvement in sentiment as limited domestic availability supported higher prices during the week. Key exporters had already pre-booked material for June shipments.

- At OMCs 19 Jun’26 chrome ore auction, 76,500 t was booked against 108,600 t offered. Bid prices increased by 1-4% m-o-m for most grades, while a few grades recorded declines of 1-2% m-o-m.

Semi finished:

- India’s semi-finished steel market witnessed a mixed trend this week, as per BigMint’s assessment. Domestic billet prices across key regions remained stable to firm, increasing by INR 50-300/t ($0.5-3/t) w-o-w. However, Gujarat, Goa, Hindupur, and Durgapur registered declines of INR 200-1,000/t ($2-10/t) during the week. Buying activity remained limited and varied across regions, as the onset of the monsoon season impacted procurement activity and steel demand. Despite subdued procurement, sellers maintained firm offer levels, anticipating that upcoming restocking activity could provide support to prices in the near term.

- The sponge iron market also recorded mixed price movements during the week. Prices in Odisha, Punjab, and southern India declined by INR 50-400/t ($0.5-4/t) w-o-w amid limited buying interest and cautious market participation. In contrast, other key producing regions remained firm, supported by modest bookings and producers efforts to maintain offer levels despite limited demand.

- On the export front, Indian DRI offers witnessed only marginal changes, due to muted buying interest from neighbouring countries. Export offers to Nepal edged lower by $2/t w-o-w to $304/t CPT Raxaul, while offers to Bangladesh increased slightly by $1/t to $312/t CPT Benapole.

- SAIL-Bokaro Steel Plant (BSL) auctioned 7,000 t of steel-grade pig iron on 17 June 2026, with the entire offered quantity sold at the base price of INR 35,600/t exw. The auction price was INR 1,450/t lower than the previous auction held on 16 May 2026, where 3,500 t out of 10,500 t offered were booked at INR 37,050/t exw. The sharp price correction encouraged buyers to replenish inventories, enabling the seller to achieve full allocation despite continued weakness in downstream steel demand.

Finished long steel:

- IF-rebar:IF-route rebar trade prices witnessed a mixed trend across major markets this week. The central region registered gains while the northern, eastern, and southern markets recorded marginal corrections amid sluggish trading activity. Buyers largely restricted purchases to immediate requirements, keeping trade volumes limited and market sentiment cautious. The price uptick in the central region was mainly driven by increased electricity tariffs in Chhattisgarh, which supported sentiment-led price hikes in the central region. However, subdued demand across regions continued to limit trade volumes and keep market sentiment cautious. Inventories across most markets stood at around 10-15 days, while dispatches remained smooth. Going forward, prices are expected to remain under pressure amid weak demand and the onset of the monsoon season.

- On a week-on-week basis, rebar prices declined by INR 100-900/t across key regions, except in the Raipur and Raigarh where the prices rose by INR 500/t and 300/t , according to BigMint’s assessment.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (1025 mm size) were assessed at INR 41,800-42,200/t exw Raipur and INR 45,000-45,600/t exw Jalna.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 43,600-44,000/t exw Raipur.

- Trade reference prices of wire rod stood at INR 42,700-43,200/t exw Raipur.

- BF-rebar:BF-route rebar prices dropped by INR 1,200/t w-o-w to INR 51,700/t exy-Mumbai, marking the lowest level in six months amid cautious, need-based procurement.

- Project bookings were concluded at INR 49,000-51,000/t landed, with buyers leveraging subdued construction activity to negotiate lower prices.

- The Mumbai BF-IF rebar price spread narrowed sharply to INR 6,000/t, down from nearly INR 10,000/t in early June, improving the competitiveness of secondary-route material.

- Distributor inventories remained elevated at over 30 days, intensifying selling pressure and limiting any meaningful price recovery.

- Market sentiment stayed weak due to sluggish demand and ample stock availability; however, ongoing infrastructure execution and relatively lower input costs could gradually support consumption in the coming weeks.

Flat steel:

-

- BigMint’s bi-weekly benchmark assessment for HRC (IS 2062, Gr E250, 2.58 mm/CTL) was assessed at INR 58,200/t ($611/t) as of 19 June, down by INR 100/t from INR 58,300/t recorded on 12 June.

- Meanwhile, the benchmark assessment for CRC (IS 513, Gr O, 0.9 mm/CTL) remained stable w-o-w at INR 65,200/t as of 19 June.

- India’s trade-level HRC prices remained range-bound during the week ended 19 June 2026, as subdued demand and cautious buying sentiment continued to weigh on market activity. Trading volumes remained limited, keeping price movements within a narrow band.

- India’s bulk imports of HRCs touched 125,919 t as on 12 June. Around 143,584 t of additional cargoes are expected by mid-July.

- India’s bulk exports of HRCs touched 61,076 t as of 12 June. Around 56,000 t of additional cargoes are expected to be shipped.

- Indian HRC export activity remained subdued during this week as markets resulted in a lack of significant export bookings, while market participants closely monitored developments amid an uncertain trade environment.