-

- EAF capacity growth continues to outpace scrap collection capacity

-

- Mills to favour secured access, discipline over price chasing

-

- Limited supply elasticity to keep downside risks contained

Morning Brief: If 2025 made one thing clear, it is that scrap supply is no longer flexible. Export controls, weather disruptions, logistics friction, and weak industrial activity steadily tightened availability, with these pressures turning structural heading into 2026.

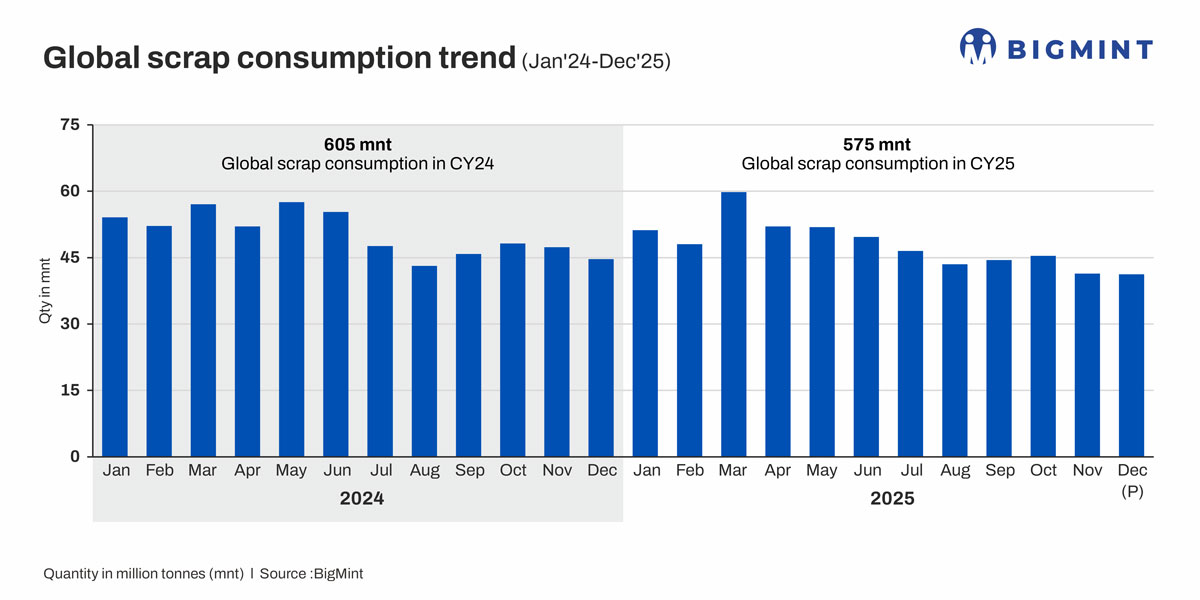

In 2025, global ferrous scrap consumption fell about 5% y-o-y to approximately 575 million tonnes (mnt), reflecting softer steel output across China, the EU, Japan, and the US. Lower utilisation masked how tight the supply side really was.

As 2026 begins, the ferrous scrap market looks structurally undersupplied, even as steel output growth is expected to remain muted. New EAF additions of around 10-12 mnt capacity — mainly in India, the Middle East, and Southeast Asia — are expected to lift scrap demand by 3-4% to around 590-600 mnt this year. However, scrap generation is unlikely to expand at an equal pace, much less exports, which could even fall due to policy constraints.

This leaves the global scrap landscape in a fundamentally tighter environment in 2026, though steel pricing, production, and profitability will ultimately dictate actual market dynamics.

Key factors influencing scrap market trends in 2026:

Export supply to tighten amid policy interventions: The EU stopped short of an outright export ban in CY’25, but oversight clearly tightened. In July, Brussels activated a customs surveillance mechanism covering ferrous and non-ferrous scrap, signalling a more interventionist stance ahead of further policy review.

Stricter European waste-shipment approvals for exports to South Asia will increase the value of certified, low-residual scrap.

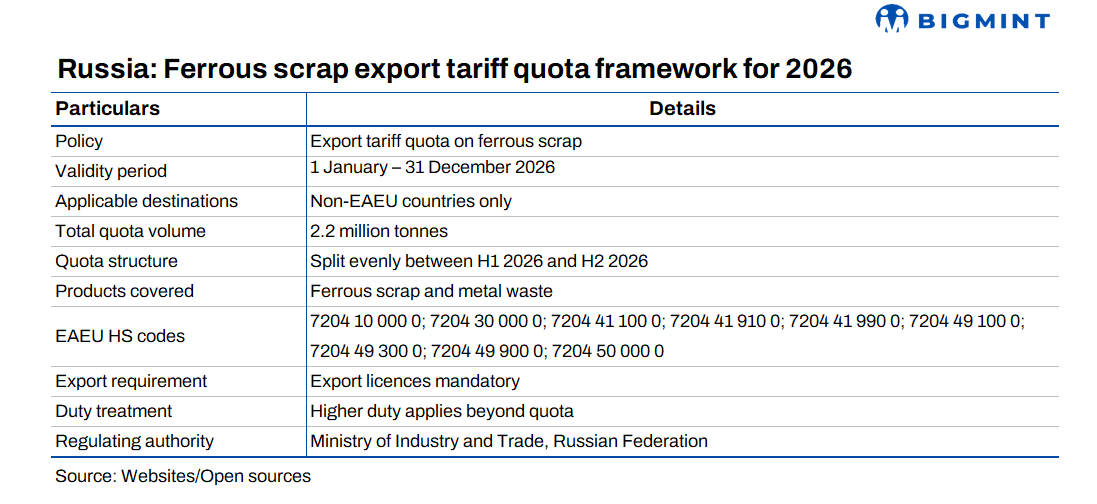

Similarly, Russia and Ukraine, besides some key exporting regions in Central Asia, had scrap export restrictions in place in 2025, and there is every likelihood that the same will persist into 2026. While a new tariff quota from January 2026 lifts Russia’s export cap to 2.2 mnt from 1.6 mnt, strict licensing and higher duties mean only marginal relief, not a supply surge.

However, even beyond stricter regulatory controls, scrap generation across Europe remains slow amid deindustrialisation and high energy costs. Ageing collection systems in Europe and weather risks across CIS regions further complicate the import landscape.

Meanwhile, in early 2026, tariff speculation ahead of a mid-2026 review encouraged stockpiling in the US, delaying export sales and tightening seaborne availability for buyers in Turkiye and South Asia.

Global steel production growth may remain subdued: With the Chinese government announcing its intention to regulate steel production further this year, growth in global crude steel production is expected to be limited. As China continues to reduce its output, global cumulative volumes may remain flat y-o-y or could even soften marginally, even as steel consumption improves from last year.

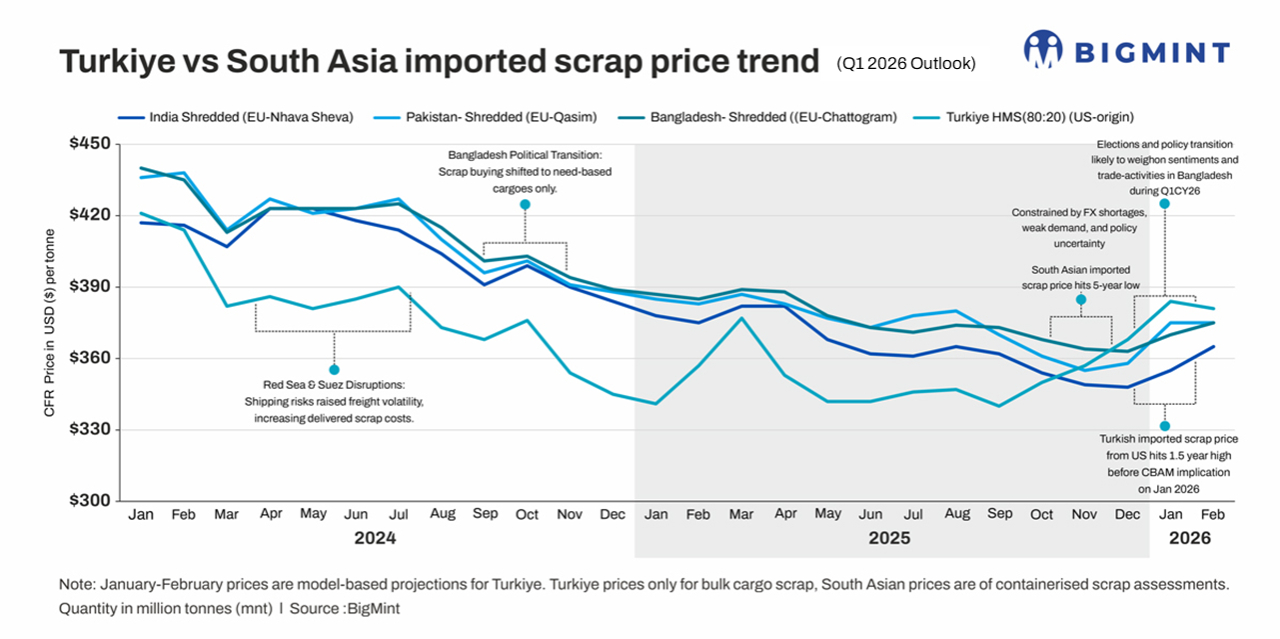

Availability of earthquake scrap changes Turkish import equation: Rising domestic scrap generation is likely to temper Turkish import demand, though the country’s structural dependence on imports is unlikely to decline.

To illustrate, in 2025, scrap imports into Turkiye, the world’s largest importer, fell around 7% y-o-y to nearly 18.6 mnt. On the surface, this looked like a demand issue, as rebar exports underperformed for much of the year, mills ran at lower utilisation, and cash flows stayed tight. However, the real surprise was an estimated 30% jump in domestic supply, driven by demolition of damaged structures following the Kahramanmaras earthquake in early 2023.

Sources suggest obsolete scrap arisings rose 20-25% in early 2025, supported by the dismantling of over 50,000 severely damaged buildings. Official estimates point to 4.5-5 mnt of additional scrap generated from these activities alone. Most of this material was heavy, obsolete scrap — rebar and structural steel — and it now accounts for around 40% of Turkiye’s domestic scrap supply.

Narrowing cost gap may keep billet imports attractive: Low-priced square billets from Asia and Russia emerged as an attractive alternative to scrap in 2025. Aggressive exporter pricing led to a narrowing cost difference between scrap-based melting and billet-based rolling.

This dynamic is likely to stay in place in Q1CY’26, with Chinese 3SP billet export offers expected to remain in the $445-455/t FOB range, as in Q4 of last year. Prices are unlikely to climb up unless downstream demand improves meaningfully, with the cost gap with scrap in Turkiye estimated at $70-80/t, particularly as imported scrap prices remain firm around $375-380/t CFR.

While tight scrap availability still provides a floor, the continued flow of low-priced billet from China is likely to keep Turkish scrap demand disciplined this year.

CBAM unlikely to create immediate demand spike: The Carbon Border Adjustment Mechanism (CBAM) is unlikely to spark an immediate scrap market frenzy, though it will boost scrap demand in the next few years. Blast furnaces (BFs) cap scrap usage at fixed levels, and any tweaks are minor percentage shifts already priced in. Over time, effects will depend on Europe’s EAF investments replacing old BFs.

Additionally, while it is expected that Turkish steel exports to the EU may gain momentum due to its low emissions production process, no significant impact has been observed yet, likely as EU safeguard measures stem inflows.

Region-wise analysis:

Turkiye: According to BigMints pricing forecast, Turkish import prices of US-origin HMS 80:20 are projected to remain firm near $380/t CFR in this quarter, with minor corrections towards the quarter-end. Prices will be supported by a seasonal supply tightness and limited availability of cheap billet alternatives.

However, mills remain cautious. Finished steel exports are uneven, domestic demand is patchy, and buyers are sticking to need-based procurement, not stock building. Stable freights and currency movements have further reduced any urgency to front-load purchases.

US: Despite constraints in scrap exports, US ferrous scrap imports are expected to rise by 5-6% in 2025, led by inflows from Mexico and Canada into the United States. Further growth is limited less by price and more by rail and trucking capacity at border crossings. Quality is tightening the supply. Mexican scrap often carries higher copper residuals, while Canadian material includes variable alloy content from automotive sources. As EAF chemistry standards rise, usable scrap availability is lower than headline volumes suggest.

Steel import tariffs support domestic steel prices but can suppress scrap demand when downstream manufacturing slows. Tariff exemptions create short-term demand swings, while globally, tariffs contribute to scrap oversupply at origin and price support in protected markets.

Logistics remain a key cost factor. About 40% of US scrap is generated in the Midwest, while demand growth is coastal, adding $30-50/t in freight. Mill inventories at 45-50 days point to a cautious balance rather than oversupply.

India: Scrap import activity in India is expected to remain muted in this quarter. Weak demand in the domestic finished steel market continues to constrain raw material buying, as steel-consuming sectors face low investment, tight liquidity, and subdued end-user demand. At the same time, steelmaking capacity additions have outpaced real market requirements, intensifying competition among mills.

Steel export challenges persist amid weakening European demand and aggressive pricing from Asian suppliers. Volatility in iron ore and energy prices, coupled with the depreciation of the rupee, has added further uncertainty to procurement decisions. Additionally, competitively priced domestic scrap, along with rising consumption of sponge iron and other metallic products, continues to limit reliance on imported scrap.

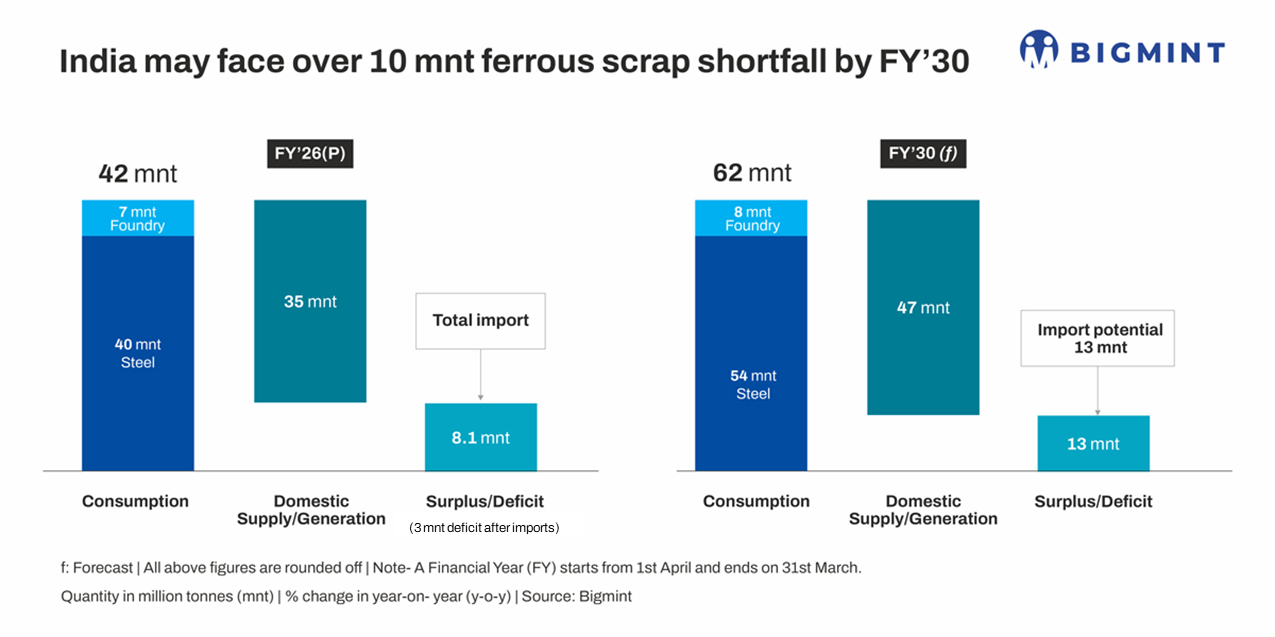

However, steel capacity expansion towards 220+mnt keeps India the main catalyst for incremental scrap demand. Imports are projected to decline to around7.8-8.1mntinFY’26 against 8.4 mnt in FY’25, while domestic collection improvements gradually raise selfsufficiency. Infrastructure incentives, EAF additions, and decarbonisation mandates will continue to underpin longterm scrap consumption growth.

However, steel capacity expansion towards 220+mnt keeps India the main catalyst for incremental scrap demand. Imports are projected to decline to around7.8-8.1mntinFY’26 against 8.4 mnt in FY’25, while domestic collection improvements gradually raise selfsufficiency. Infrastructure incentives, EAF additions, and decarbonisation mandates will continue to underpin longterm scrap consumption growth.

Broader market outlook:

As we step into 2026, the mood across the ferrous scrap market is cautious rather than pessimistic. Most participants agree that the first quarter will be slow, but there is also a broad sense that the market is laying the groundwork for a more stable second half.

Asian imported scrap demand is expected to remain subdued through winter, with India and Vietnam showing little urgency to increase purchases amid weak steel demand and comfortable inventories.

In 2026, US-origin scrap prices are less about how much scrap is around and more about what kind of scrap it is–and how easily it can move. Mills are paying up for material that meets tighter specs and can be delivered reliably, while lower-quality or poorly positioned tonnage is losing relevance.

On pricing, HMS (80:20) CFR Trkiye is generally expected to trade in a $380-420/t range this year. What really stands out, though, is the growing gap within the market. Certified, low-residual scrap–especially material suitable for green steel–should increasingly attract premiums. Europe is likely to stay relatively flat on dockside prices, while South Asia will continue to look to Turkish benchmarks, largely because DRI-scrap parity keeps pulling prices back to that reference point.

In the near term, Q1 is widely seen as a period of consolidation rather than recovery. Vietnam steelmakers are not expected to rush into new scrap bookings before winter ends. With domestic scrap already covering around 45-50% of steel output and inventories comfortable for roughly one month of operations, there is little urgency to step up imports.

In the near term, Q1 is widely seen as a period of consolidation rather than recovery. Vietnam steelmakers are not expected to rush into new scrap bookings before winter ends. With domestic scrap already covering around 45-50% of steel output and inventories comfortable for roughly one month of operations, there is little urgency to step up imports.

Still, the bigger picture in Vietnam remains constructive. Scrap imports totaled 5.3-5.4 mnt in January-December, up 18-20% y-o-y helped by government-backed infrastructure projects and stronger long steel production.

In India, secondary mills are still under pressure, and scrap buying is likely to stay cautious through the first quarter. But there is confidence that from Q1 onward, as construction activity revives and project execution picks up, demand will normalise.

In Bangladesh, elections and policy transition are weighing on sentiment, keeping Q1 quiet. The real test will be Q2 — if infrastructure spending restarts, scrap demand should follow.

Pakistan faces a seasonal lull in February and March due to Ramadan and Eid, but post-Eid restocking is expected to improve market activity. Beyond the first quarter, the conversation turns more constructive. Inventories are already thin, and the market has very little buffer. That means any improvement in steel demand could quickly tighten scrap availability, pushing prices higher without much warning.

The biggest wildcard remains Europe. CBAM comes into force from January 2026, and there is still a lot of uncertainty around how embedded emissions will be treated and whether further scrap export restrictions could be introduced. Many in the market feel Europe could surprise in 2026 — either through stricter regulation or policy shifts that reshape trade flows.

With inventories low and policy risk high, 2026 looks less about volume growth and more about discipline, positioning, and adaptability.