India’s evolving end-of-life vehicle recycling ecosystem and scrap generation potential

-

- RVSF capacity has expanded but utilisation remains low at only 4050%

-

- OEM-led, fleet-based scrappage programmes critical to improving ELV inflows

Indias registered vehicle scrapping infrastructure has expanded steadily over the past three fiscal years, with FY25-FY26 marking a clear acceleration phase. The sharp rise in Registered Vehicle Scrapping Facilities (RVSFs) reflects faster on-ground implementation of the Vehicle Scrappage Policy and growing participation from organised and OEM-backed players. However, capacity creation is currently running ahead of actual end-of-life vehicle (ELV) inflows, indicating that the ecosystem remains in a build-out and positioning phase.

Tier-1 players accelerate RVSF expansion:

Tier-1 automotive OEMs and organised recycling players are rapidly scaling up their presence in Indias Registered Vehicle Scrapping Facility (RVSF) ecosystem, driven by tighter policy enforcement and long-term confidence in end-of-life vehicle (ELV) generation. OEM-backed and large organised players such as Maruti-Toyotsu India, Tata Motors Re.Wi.Re, Mahindra MSTC Recycling, and CERO Recycling are leading capacity expansion through multi-location rollouts and state-wise MOUs, with a strong focus on Uttar Pradesh, Haryana, Gujarat, Maharashtra, and select northern states.

These players are prioritising early capacity creation, strategic land acquisition, and compliance-led infrastructure, positioning themselves ahead of the expected rise in ELV inflows over the medium term. While current utilisation levels remain modest, Tier-1 companies are leveraging OEM sourcing networks, insurance partnerships, and integrated logistics models to build scalable operations. This organised expansion underscores a clear shift away from informal dismantling towards a regulated, traceable, and circular vehicle scrapping ecosystem.

Perspectives of industry participants:

The growing footprint of Tier-1 players is driving formalisation in Indias vehicle scrapping market. While RVSF capacity has expanded rapidly, utilisation remains low at only 40-50%, as ELV availability continues to lag behind newly added capacity. OEM-linked recyclers, fleet operators, and organised RVSFs stand to benefit from structured sourcing, fleet scrappage programmes, and clearer inter-state movement protocols.

Industry participants flag key challenges, including a shortage of skilled labour and limited government-led initiatives. Tata Re-Wi-Re officials emphasise that stronger government intervention is critical, with authorities encouraged to lead by example by deregistering and dismantling Govt. vehicles through authorised RVSFs. Such measures would improve ELV supply visibility, increase capacity utilisation, and accelerate market formalisation.

As the ELV ecosystem matures, organised operators are poised to retain a structural advantage through higher utilisation, regulatory compliance, and stronger market positioning.

Concentration of RVSFs across key states:

Indias registered vehicle scrapping infrastructure remains highly concentrated, with Uttar Pradesh leading at 85 RVSFs, accounting for nearly 45% of the national total. Haryana follows with 22 facilities (around 12%), supported by strong logistics access and proximity to auto clusters.

Gujarat, Maharashtra, and Madhya Pradesh together contribute a meaningful share, while Chhattisgarh has emerged as a notable mid-sized contributor. Overall, the top six states account for over 73% of Indias total RVSFs, underscoring a skewed regional distribution and highlighting significant expansion potential in under-penetrated southern and eastern markets.

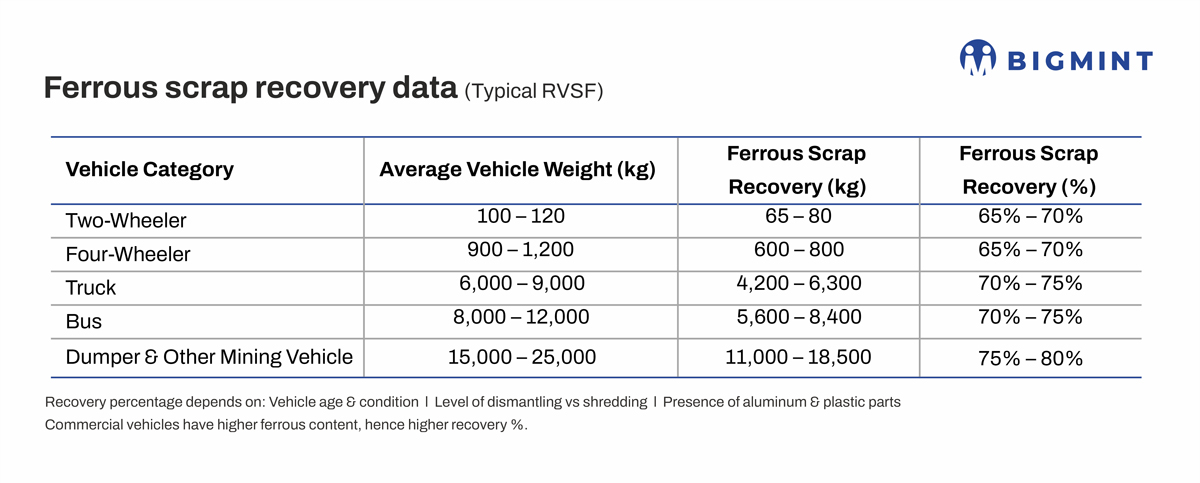

Ferrous scrap recovery rates across vehicle types:

Ferrous scrap recovery varies by vehicle type, with two-wheelers recovering 65-70% of their 100-120 kg weight as ferrous metal. Four-wheelers show similar recovery rates but with higher weights. Commercial vehicles like trucks and buses have higher recovery rates of 70-75%, while heavy mining vehicles achieve the highest at 75-80%, due to their greater ferrous content. Recovery depends on vehicle condition, dismantling methods, and presence of non-ferrous parts.

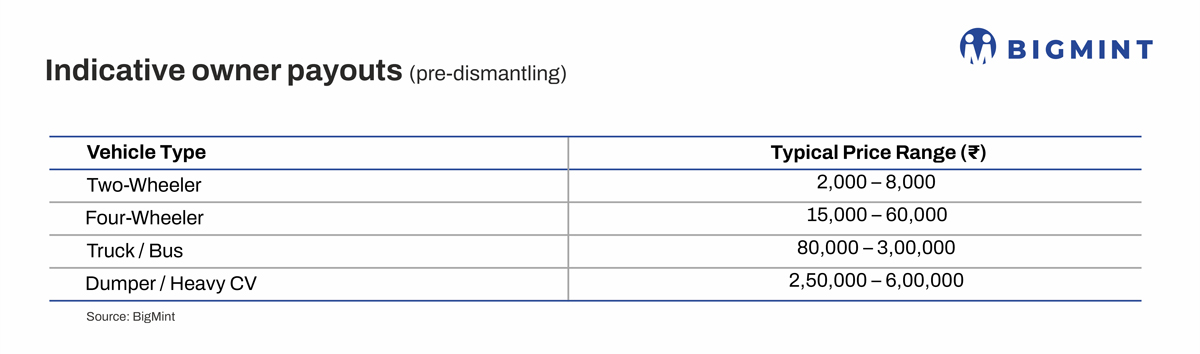

RVSF vehicle pricing for owners:

Before dismantling, vehicle owners are offered a scrap/buyback price by the RVSF. The price depends on:

Vehicle type & age -Two-wheelers, four-wheelers, commercial vehicles (truck, bus, dumper) have different base rates.

Vehicle condition -Functional vs non-functional, presence of reusable parts.

Metal composition -Higher steel content vehicles fetch more; aluminium and other metals are valued separately.

Market rates -Ferrous and non-ferrous metal prices at the time influence the offered price.

Vehicle owners receive the payment within 10-15 days after RC de-registration is completed, ensuring transparency and formalisation of the transaction.

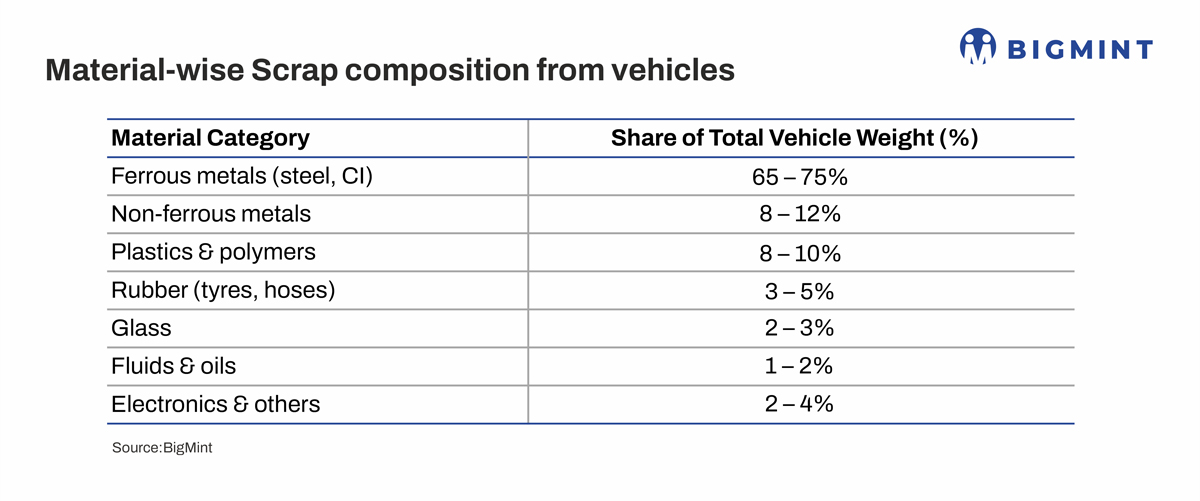

Types of materials recovered from ELVs:

Ferrous metals account for nearly 65-75% of vehicle scrap by weight, driving volume recovery at RVSFs, while non-ferrous metals-though only 8-12% play a key role in value realisation. Organised operators benefit from efficient segregation, improving overall recovery economics as ELV volumes scale up.

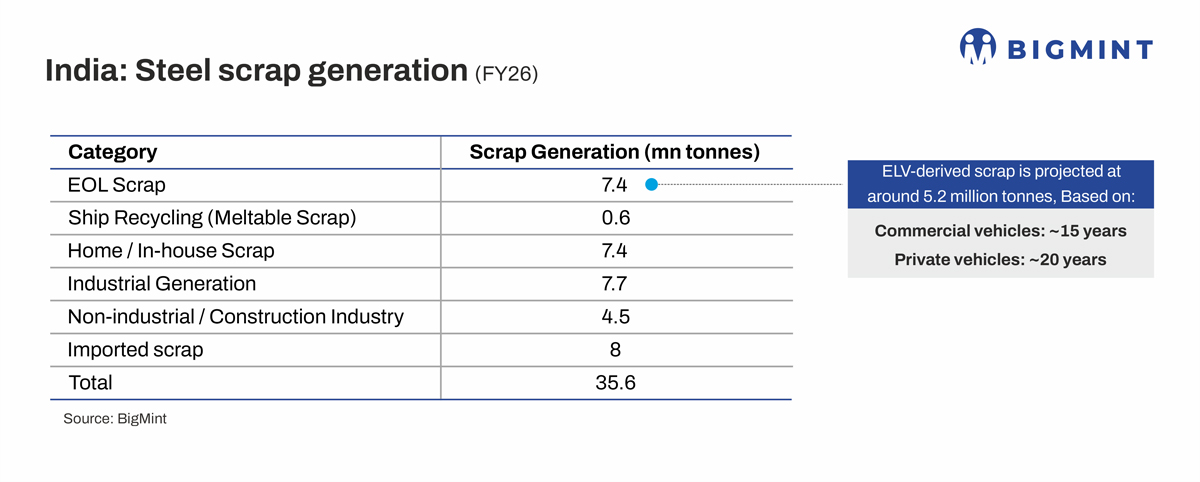

ELVs emerging as a key contributor to Indias scrap supply:

End-of-life vehicles (ELVs) are emerging as a significant contributor to Indias scrap ecosystem, accounting for approximately 5.2 mnt-70% of the 7.4 mnt of EOL scrap-out of the total 35.6 mnt of scrap generated in FY25. While industrial, home/in-house, imported, and ship-recycled scrap remain major sources, ELVs are increasingly becoming a key feedstock for steelmakers.

However, market participants indicate that near-term relief in scrap availability from the scrappage policy is unlikely, as ELV-based scrap volumes have yet to reach commercially significant levels.

Policy shortfalls in incentivising vehicle scrapping:

Indias vehicle scrappage policy is largely penalty-driven, with limited financial incentives for private vehicle owners who form the bulk of ELVs. Inconsistent state-level benefits, weak deregistration enforcement, and lack of uniform inter-state ELV movement rules have kept organised scrappage volumes below potential, despite rapid RVSF capacity addition.

Targeted policies to incentivise higher scrapping:

Market participants believe that higher scrappage levels can be achieved through direct financial incentives for voluntary scrapping, particularly for private vehicles, along with uniform deregistration and inter-state ELV movement rules to ease organised sourcing. In addition, stronger OEM-led and fleet-based scrappage programmes are seen as critical to improving ELV inflows and supporting sustainable utilisation of RVSF capacity.

GST rationalisation may improve margins for organised recyclers in the short term but is unlikely to materially lift ELV volumes immediately. In the medium term, lower transaction costs could accelerate the shift of ELVs from informal to formal channels, supporting higher RVSF utilisation.

Potential impact of BS VI and BS VII (from FY27):

Tightening emission norms under BS VI, followed by the expected BS VII rollout from FY27, are likely to increase compliance and maintenance costs for older vehicles, particularly in metro markets such as Delhi-NCR. Stricter pollution checks, usage restrictions, and higher upgrade costs are expected to accelerate scrappage decisions, especially for ageing commercial fleets and high-usage private vehicles. As a result, metros are likely to act as early demand centres for ELV scrapping, supporting higher utilisation of organised RVSFs over the medium term.

Outlook:

Indias end-of-life vehicle (ELV) recycling ecosystem is transitioning from a capacity build-out phase to a demand-led growth phase, though the shift will be gradual. While RVSF infrastructure has expanded rapidly and organised, OEM-backed players are well positioned, near-term ELV scrap inflows are expected to remain below installed capacity due to limited incentives, uneven state-level execution, and longer effective vehicle life cycles-particularly for private vehicles.

Over the medium term, tighter emission norms under BS VI and the expected BS VII regime from FY27, especially in metro markets such as Delhi-NCR, are likely to act as stronger catalysts for scrappage. Combined with improving policy clarity, GST rationalisation, and stronger OEM- and fleet-led sourcing programmes, ELV-derived scrap volumes are expected to accelerate meaningfully, supporting higher RVSF utilisation and increased formalisation. BigMint expects organised recyclers to gain a structural advantage as ELV availability improves, strengthening domestic scrap supply and reducing reliance on imports over the next decade.