India’s non-coking coal imports fall by 6% y-o-y in CY’25. Know why?

-

- Coal imports decrease by over 10 mnt y-o-y

-

- CY’25 coal-fired power generation drops for 2nd time in 50 years

-

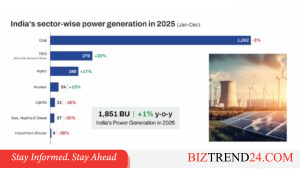

- Non-fossil power production rises sharply in CY’25

Morning Brief: India’s imports of non-coking coal, used in power generation and in the industrial sector, declined by 6% y-o-y in CY’25, as per latest BigMint data. Imports dropped to around 163 million tonnes (mnt) from over 173 mnt in CY’24.

Total non-coking coal imports began on a sedate note with 13 mnt in January but climbed to a peak of 18 mnt in May before falling sharply to around 11.4 mnt by December. The decline in non-coking coal imports was due to the following reasons:

Historic drop in coal-based power generation: India’s power generation from coal dropped 3% y-o-y in CY’25 on a milder summer and prolonged monsoon keeping demand for air-conditioning low, which showed a decline of 9.8% compared to CY’24. This is only the second time in over 50 years that coal-fired power generation has fallen for a full year, based on a time series of coal-fired power generation starting from 1971 prepared by the International Energy Agency (IEA). Therefore, demand for coal imports for power remained muted.

Sharp growth in renewable power: Alongside the de-growth in thermal generation, renewable generation rose sharply – over 22% y-o-y for solar, wind and small storage combined and around 15% for large hydro. Total power generation from coal and gas increased at an average rate of 63 terawatt-hours per year (TWh/year) from CY’19 to CY’24, and fell by 50 TWh/year from CY’24 to CY’25, data from the Centre for Research on Energy and Clean Air (CREA) show. In contrast, non-fossil power generation increased at an average rate of 22 TWh/year from CY’19 to CY’24, speeding up to 71 TWh/year from CY’24 to CY’25.

These two factors ensured lower demand for imported coal despite the marginal 1.06% y-o-y increase in domestic coal production, which reached around 984 mnt in CY’25, as per BigMint data.

Port-wise imports:

Coal imports declined sharply at ports along the eastern coast ports amid improved domestic supply. In percentage terms, several east coast ports recorded a 30-50% decline in import volumes from their 2025 peaks by year-end.

This east coast trend closely mirrors rising domestic coal availability from CIL subsidiaries in Odisha, Jharkhand and West Bengal, where shorter rail distances, higher mine output and improved evacuation enabled indigenous coal to competitively displace imports for power and industrial consumers along the eastern seaboard.

In the west coast, too, non-coking coal imports declined in 2025 but more mildly and less uniformly than the east coast. Mundra saw a sharp contraction, while Kandla/Tuna ended the year below mid-year peaks despite volatility. The softer decline reflects logistical constraints and higher costs of moving domestic coal to western markets.

Country-wise imports:

Indonesia remained India’s largest supplier of non-coking coal throughout 2025, followed by South Africa, the United States and Russia. While Indonesia remained the primary supplier, a marked reduction in Indonesian cargoes during the second half underscored active substitution by domestic coal rather than a mere shift in sourcing.

However, a reduction in Indonesian volumes was not offset by increased shipments from alternative origins, leading to a net drop in imports.