Global non-coking coal trade shrinks by roughly 4% y-o-y in Jan-Nov’25 – BigMint report

-

- Lower China, India demand affects global trade

-

- Dented profits, weakening prices impact Indonesian exports

-

- Outlook hazy due to regulatory pressures, energy transition

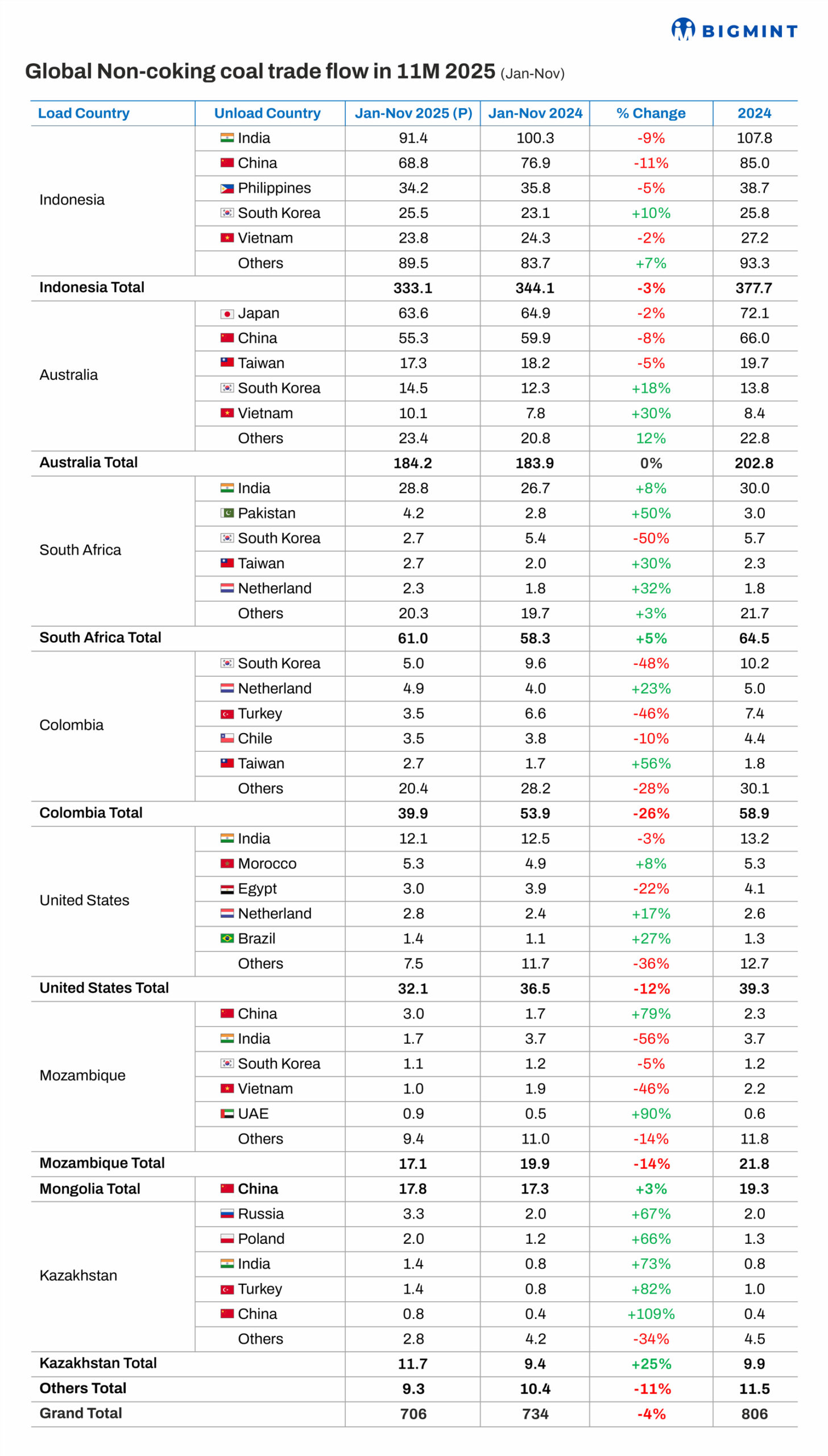

Morning Brief: Global non-coking coal trade in the January-November 2025 (11MCY’25) period declined by roughly 28 million tonnes (mnt) to approximately 706 mnt from 734 mnt in 11MCY’24, as per provisional data with BigMint.

Global trade volume declined by 4% during the period as China and India, the world’s top thermal coal consumers, reduced imports, as did other Asian majors, due to an uptick in domestic production in China and India and the gradual transition from thermal coal to cleaner energy sources for electricity production.

China and India (with the exception of rising Southeast Asian economies such as Vietnam) is the mainstay of global thermal coal trade what with Japan and South Korea hurtling at a breakneck pace to decarbonise their power systems. News of retirements of coal fleets is frequent as are government vows of total coal phase-out even before 2040.

But demand from China and India have been muted due to:

-

- Higher domestic coal production and rising inventories

-

- Rapid renewable energy buildout in both countries

-

- Lower thermal generation in India due to weather-related reasons

On the other hand, declining thermal coal prices globally, higher operating costs of running mines, and weather disruptions took a toll on exports by the leading suppliers – Indonesia and Australia.

Top exporters:

Indonesia: Indonesian coal shipments declined by around 3% y-o-y in 11MCY’25. Exports fell to a three-year low, snapping continued y-o-y increases over the past two years, mainly due to reduced demand from major importers, China and India. Exports to China and India, which together account for around 60% of Indonesias coal trade, have declined as both countries expand renewable energy and strengthen domestic supply.

Moreover, according to Badan Pusat Statistik (BPS), Indonesia, the average coal export price decreased 14% y-o-y in H1CY’25. Oversupply in global markets has pushed prices down, reduced company profits, and weakened state revenues impacting coal exports, not to mention prolonged wet weather affecting exports.

For 2025, as per the International Energy Agency (IEA), Indonesian coal production is expected to decline, bringing total production down to approximately 735-740 mnt. Producers are facing challenges due to lower prices and oversupply in the low- and mid-CV coal segments, as their main markets – China and India – are requesting lower volumes.

Australia: Australian exports recovered toward the end of the year from early jolts to post a marginal 0.2% growth in 11MCY’25. In 2025, sustained pressure from lower benchmark prices combined with a rising cost structure and weather-related port and rail disruptions led to tightened margins and amplified the sensitivity of supply to short-term shocks. Forecasters have reduced export expectations due to prolonged wet weather and softer prices, while congestion and repeated weather-related stoppages at Newcastle raised vessel queues and turnaround times, delaying shipments and complicating mine scheduling.

Dim demand from Japan for 6000 kcal/kg Newcastle coal and lower shipments to China of the 5,000 kcal/kg high-ash variety affected exports, although colder-than-average weather in South Korea led to a slight uptick in shipments from Australia. Also, prompter deliveries of lower-priced Indonesian coal after the cessation of weather disruptions affected Australias prospects.

South Africa: Coal production in South Africa is estimated to remain almost stable compared with 2024. Supply-side dynamics are shaped by infrastructure and investment decisions. Rail performance improved after Transnet implemented recovery measures and allowed private operators to use its network, which could add up to 10 mnt/year of export capacity over the next three years, as per the IEA.

The government’s financial guarantee recovery plan has stabilised Transnet’s finances, reducing operational risks. Mining companies such as Thungela reported higher output in the first half of the year, supported by better rail availability. This accounts for the increase in South African coal exports.

Colombia, US: Colombian coal supply in 2025 is estimated to decline by 18% in 2025, with exports constrained by logistical disruptions and producer curtailments. The Cerrejn mine saw multiple days of halted rail operations due to blockades and bomb attacks, reducing effective export capacity. Also, major producers adjusted mine plans in response to weaker seaborne pricing: Cerrejn cut 2025 output by 5-10 mnt, while Drummond signalled reductions to optimise operations. These factors, combined with softer thermal coal benchmarks, weigh on exports.

Similarly, muted seaborne pricing and weak demand from India saw US exports shrinking by around 12%.

Outlook:

The IEA expects that after years of growth, global coal trade (including met coal) is expected to decline by 5% in 2025, reversing the previous upward trend. Thermal coal trade is set to decrease by 6% – mainly driven by China and India.

Overall, the thermal coal trade outlook in 2026 is clouded due to:

-

- Upcoming Indonesian coal export tax

-

- Surging methane emissions from mining and regulatory crackdown in key countries

-

- Possible ban on thermal coal exploration in Colombia

-

- Fast decreasing exploration spending in Australia and the US

-

- Rapid expansion of LNG capacity worldwide and further pressure on coal prices amid regulatory tightening

- Surge in renewable electricity generation